Three Keys for a Happy Retirement

Simon Barcelon

.21 Oct 2021

.3 Min Read

Canadians spend a lifetime planning to retire, but when they do, many struggle to find happiness. Here are a few suggestions on how to fix that.

How many times while you were working did your attention drift away to fantasies about what you would do when you retired? Maybe you dreamed about travelling back home to your motherland, finally learning guitar, spending more time with your grandkids, or hosting lavish dinner parties for family and friends.

But plans aside, once retired, many Canadians start thinking of retirement as a challenge rather than the opportunity it really is.

Whether you’re currently retired or it’s just around the corner, here are three things to consider that may help you fully enjoy this chapter in your life’s story.

1. Find Fulfillment

After the initial excitement of living a life of perpetual Saturdays wears off, some retirees may struggle with feeling a lack of purpose in their lives. Filling your time with something meaningful, whether that’s pursuing a new hobby or volunteering in your community, is key to enjoying retirement. In Japan, they refer to this concept as finding your “ikigai,” and living by this ideology is believed to contribute to the exceptionally long lives of many Japanese people.¹

At Purpose Investments, we believe “ambition never retires.” Just because you’ve stopped working doesn’t mean you've retired your interests, your dreams, or your hunger to make an impact. Because of this, we created the Longevity Pension Fund, the world’s first income-for-life mutual fund, to financially empower Canadians to thrive in retirement and reach their post-work goals.

2. Keep Busy

Whenever we think about retirement, another word often comes to mind: relaxing. You worked hard your entire life to reach this point, so you may want to step back from the daily grind to relax and enjoy life. But relaxing doesn’t necessarily mean the same thing to everyone! We suggest filling your time with everything you’ve ever wanted to do: that may mean taking that trip you always put off, learning that new skill you never had the time to do before, or just simply relaxing with your favourite author.

3. Secure an Income for Life

This is fundamental for many: making sure your money lasts as long as you do. If you want to make the most of your retirement, it helps to have the confidence in your financial situation to do so. As Oscar Wilde once famously said, “It is better to have a permanent income than to be fascinating.”

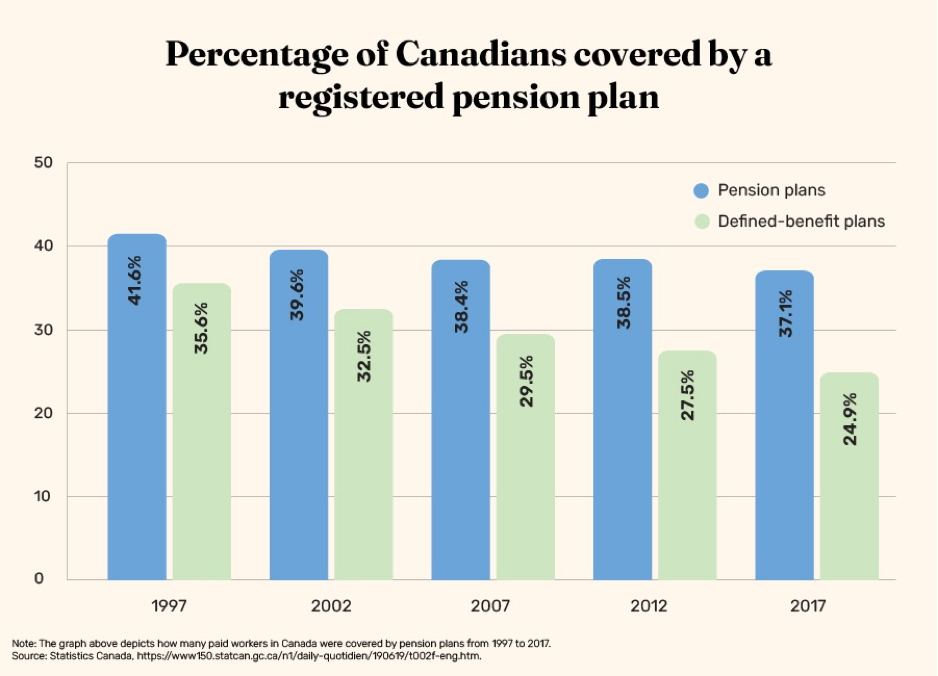

However, with pension plans seemingly falling out of fashion,² many retirees worry about sustaining a lifetime income. What used to perhaps be the hardest step here is now the easiest as Longevity was designed to act like a pension for everyone. Studies show a person’s retirement satisfaction drastically increases when they have the comfort and security of a lifetime income stream through a defined benefit pension plan.³ You can rest easy knowing you have secured an income for life with Longevity!

To find out how to plan for a better next chapter with Longevity, visit RetireWithLongevity.com or reach out at contact@retirewithlongevity.com.

1. “The Philosophy of Ikigai: 3 Examples About Finding Purpose” Positive Psychology. https://positivepsychology.com/ikigai/

2. “Percentage of paid workers covered by a registered pension plan” Statistics Canada, June 2019. https://www150.statcan.gc.ca/n1/daily-quotidien/190619/t002f-eng.htm

3. “What makes retirees happy?” Center for Retirement Research at Boston College, February 2005. https://dlib.bc.edu/islandora/object/bc-ir:104470

The Fund has a unique mutual fund structure. Income in the form of Fund distributions is not guaranteed, and the frequency and amount of distributions may increase or decrease. Most mutual funds redeem at their associated Net Asset Value (NAV). In contrast, redemptions in the decumulation class of the Fund (whether voluntary or at death) will occur at the lesser of NAV or the initial investment amount less any distributions received. You can always access the lesser of unpaid capital (initial value of your investment less any income payments made) or your net asset value. Fees may apply.

Commissions, trailing commissions, management fees and expenses all may be associated with the Longevity Pension Fund. This communication is not investment advice, nor is it tailored to the needs or circumstances of any specific investor. Talk to your investment advisor to determine if the Longevity Pension Fund is suitable for you and always read the prospectus before investing. There can be no assurance that the full amount of your investment in a fund will be returned to you. Investments in the Fund are not guaranteed, investment values in the Fund change frequently and past performance may not be repeated.

The information contained in this article was obtained from sources believed to be reliable; however, we cannot guarantee that it is accurate or complete. This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters