How to Help Plan Members Navigate Their Finances After Retirement

Longevity Team

.24 Jun 2021

.5 Min Read

In Canada, there is no shortage of structures, plans, and programs to help plan members in the accumulation phase map their financial journeys to retirement. However, that changes after retirement, leaving many Canadians to fend for themselves when it comes to figuring out how to make their savings last.

The problem of decumulation results from retirement savings plans that don’t consider what happens to plan members after they retire. Offering solutions for only half of the financial journey has contributed to high levels of insecurity and anxiety related to retirement in Canada.

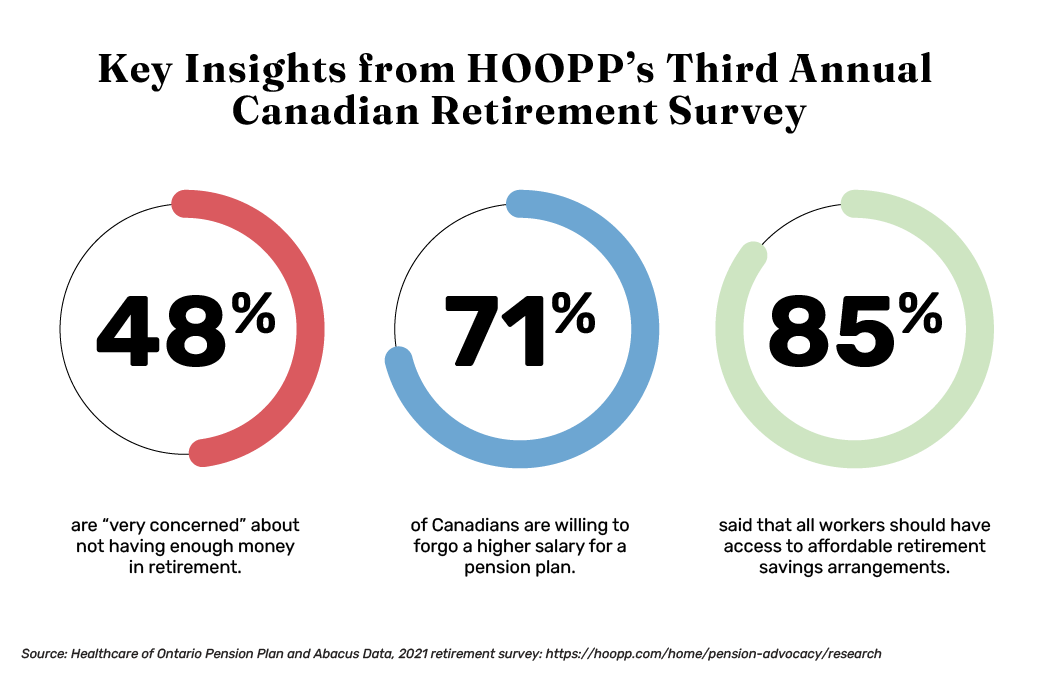

In May, the Healthcare of Ontario Pension Plan (HOOPP) released results from its 2021 Canadian retirement survey. The survey results speak to just how prevalent the problem of retirement income insecurity is to all Canadians, despite their income level.

Offer a Retirement Plan That Helps Plan Members Throughout Their Financial Journey

As a plan sponsor, offering a comprehensive solution that supports plan members in both phases of their financial lives (pre- and post-retirement) is a great way to distinguish yourself as an employer and help plan members in ways meaningful to them.

However, improving the financial wellness of plan members goes above and beyond offering retirement and pension plans. The next step companies should take to combat the retirement crisis and improve the financial wellness of their employees is making sure plan members look at retirement as an exciting opportunity instead of a challenge.

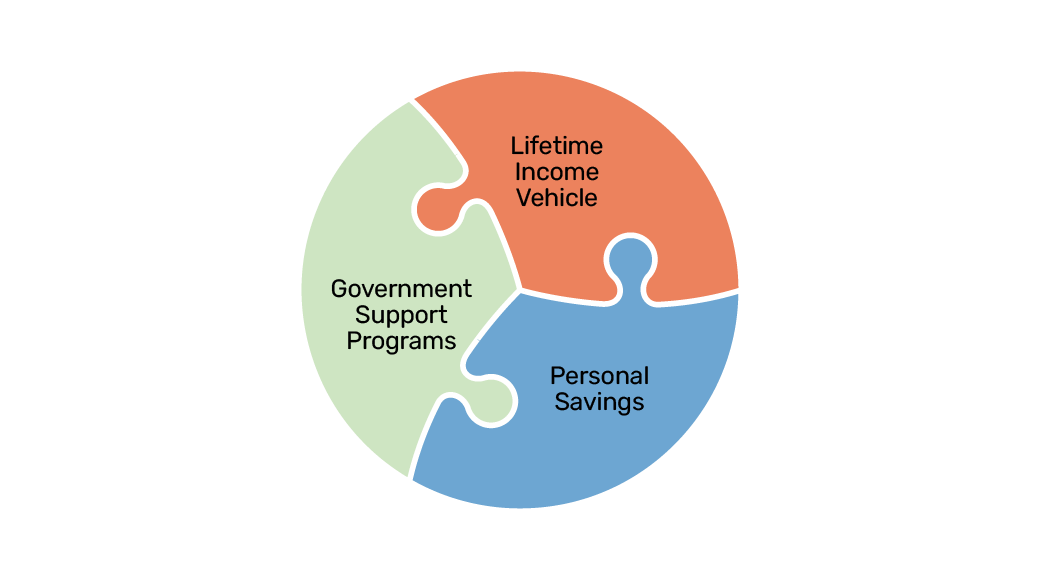

As a plan sponsor, you can pave a new path for Canadians to navigate and thrive in their post-work years by educating plan members on three core components of a retirement savings plans.

Teach Plan Members Three Components of a Strong Retirement Plan

1. Government Support Programs

It is crucial that plan members are aware of the government support programs available to them after they retire.

Government support programs like the Canadian Pension Plan (CPP), the Quebec Pension Plan (QPP), and Old Age Security (OAS) are available to Canadians once they reach a certain age.

The CPP is a monthly taxable benefit that Canadians can receive for the rest of their life once they are 60 years old, provided that they, or a former spouse or common-law partner from whom they've received credits, made at least one contribution to the CPP while working. Monthly payments vary, but according to the Government of Canada website, the average CPP payout in January 2021 was $619.75.2

The QPP is a public insurance plan for workers in Quebec who are 18 and older and whose annual employment income is greater than $3,500. Its purpose is similar to the CPP, providing basic financial protection in the event of retirement, death, or disability.3

The OAS is a government program you become eligible for when you turn 65. According to the website, the maximum amount someone can receive from OAS is $618.45.4

CPP, QPP, and OAS are foundational components of retirement income. However, while these programs create a good starting point, together, they aren’t enough to provide for most people’s needs. It’s important that your plan members know they will likely need to rely on additional income streams to sustain their lifestyle in retirement.

2. Personal Savings

A plan member’s personal savings is another core component of a retirement savings plan. Encourage plan members to talk to a financial advisor about investing their savings in a discretionary portfolio that matches their risk tolerance and financial goals.

Personal savings supplement government pension programs and allow more breathing room in a budget that will allow your plan members to really enjoy retirement. In fact, many plan sponsors are now considering offering independent financial advice to their members once they are ready to retire. Additionally, many record keepers offer the ability to provide financial advice to members as part of the group arrangement at no additional cost.

3. Lifetime Income Vehicles

A common worry for Canadians is whether they will run out of money in retirement. Easy ways to help alleviate this fear for plan members is by educating them on lifetime income products.

An annuity is a well-known lifetime income product issued by an insurance company that plan members can pay for upfront, and then receive a fixed income stream for the rest of their life. The guaranteed income stream helps ease the worry that a person might run out of money before they die.

However, annuities often lack flexibility— typically, the purchase is a permanent decision where you no longer have access to your capital once you buy the annuity, and payments are generally fixed and don’t grow over time.

However, there are alternatives to annuities that offer more flexibility and higher expected returns. At Purpose Investments, we recently launched the Longevity Pension Fund, a new income-for-life solution that provides income for life like an annuity but structured as a mutual fund, allowing investors the flexibility to redeem their investment (at the lesser of its current net asset value, or their initial investment less any received distributions) and the potential for higher income distributions as a person ages. Learn more about how the Longevity Pension Fund differs from an annuity here.

Two Ways Plan Members Can Invest in the Longevity Pension Fund

1. The Accumulation Class

As a plan sponsor, you can add the Longevity Pension Fund to your product suite as a defined-contribution savings plan for your employees, providing plan members a defined-contribution option that offers lifelong support by helping them save while they’re working then automatically transitioning to providing lifetime income when they turn 65.

2. The Decumulation Class

Alternatively, if your plan members already have a defined-contribution plan they are using to help save for retirement, but would like a more flexible alternative to an annuity to provide income for life, they can invest in the Decumulation Class when they are 65 or older. The Longevity Pension Fund can be sheltered in a group plan like a DCPP or RRSP and is designed to provide monthly income distributions starting at 6.15% for a 65-year-old. For information on how a plan member would receive income for life in retirement, please refer to the case study here.

We believe lifetime income products should be a core component of every retirement savings plan. If you would like to help your plan members successfully navigate retirement and want to learn more about the Longevity Pension Fund, please reach out at contact@retirewithlongevity.com.

1. Healthcare of Ontario Pension Plan and Abacus Data, 2021 retirement survey: https://hoopp.com/home/pension-advocacy/research

2. “CPP Retirement Pensions,” the Government of Canada: https://www.canada.ca/en/services/benefits/publicpensions/cpp/cpp-benefit/amount.html

3. “The Role of the Employer and the Québec Pension Plan,” the Gouvernement du Québec: https://www.rrq.gouv.qc.ca/en/employeur/role_rrq/Pages/role_rrq.aspx

4. “Old Age Security,” the Government of Canada: https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/benefit-amount.html

The content of this document is for informational purposes only, and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained on this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice and neither Purpose Investments Inc. nor is affiliates will be held liable for inaccuracies in the information presented.